Consumer Apps Have a Long Way to Go

The consumer app hype is not all it is cracked up to be. It is certainly true that app revenue has taken off and now exceeds games revenue. Yet, broken down by winners, the growth looks more like an app-store onshoring trick than a new consumer-app growth machine: entertainment subscriptions, a productivity wave that is mostly AI, and a residual "Other" bucket that still has not shown the speed of scale or LTV depth of traditional games.

Without that, games will keep dominating VC funding. The great challenge for apps is to create repeatable revenue loops that let them win ad auctions, scale paid acquisition, drive downloads, grow users, and increase revenue. Like games, winners are paid on revenue multiple potential, not straight profit.

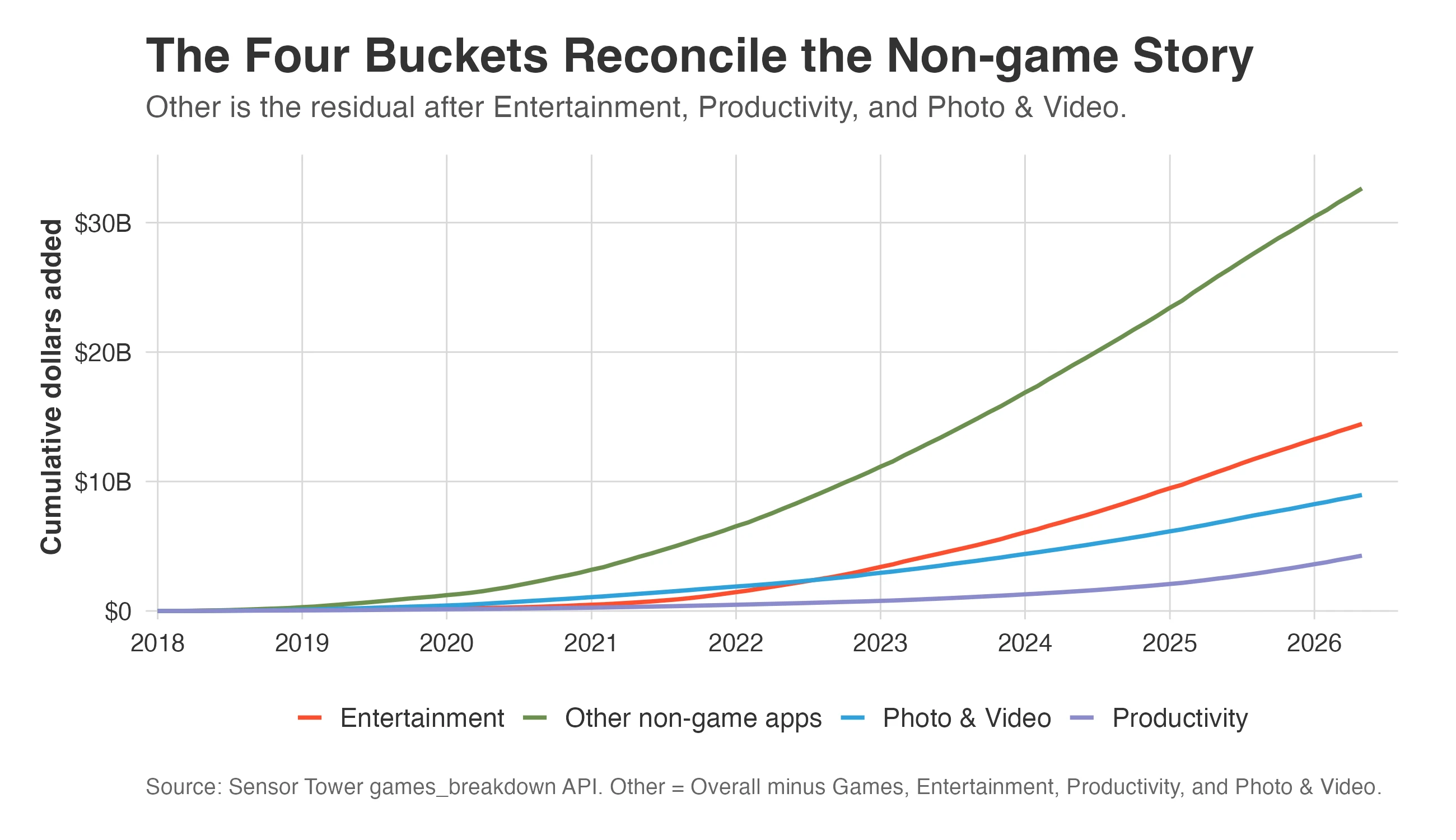

Nearly all consumer-app growth has come from Entertainment, Photo & Video, Productivity, and "Other." Other is not Education. It is the residual non-game bucket after Entertainment, Productivity, and Photo & Video are removed.

For each category, we can rank the top apps that are actually driving growth. That is where the hype starts to look thinner.

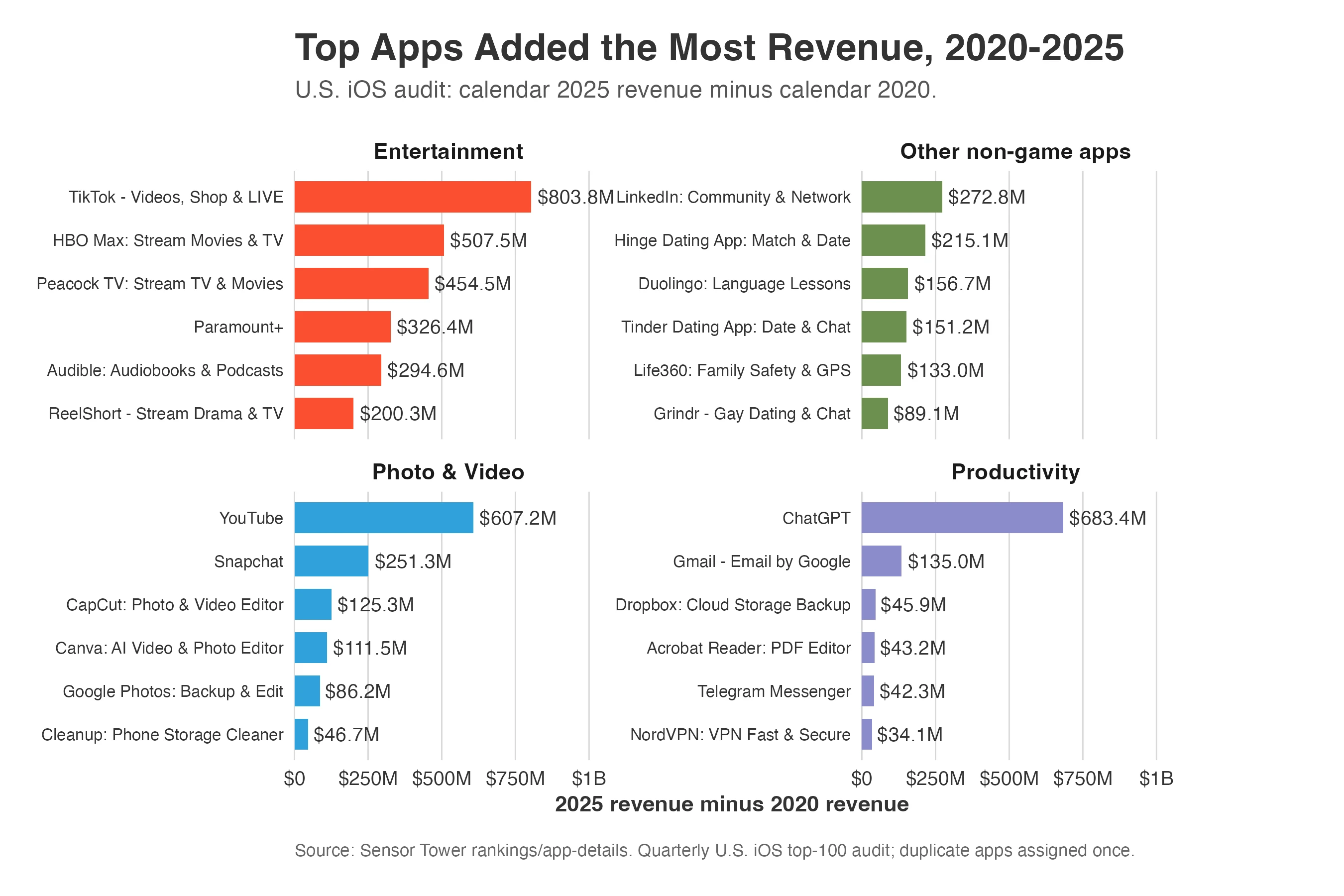

Entertainment breaks down almost exactly as expected. The vast majority of growth is driven by the onshoring of entertainment apps like Paramount+ and Peacock, not by mobile-native consumer favorites like Tinder or Duolingo. ReelShort is the interesting exception we should talk about, because it looks closer to a native mobile entertainment format. But the broader mechanism is simple: big media players using in-app subscriptions.

Consumers do not pay for Productivity. End of story. The category is not a broad productivity renaissance. It is ChatGPT, a few platform incumbents, and a long tail that does not change the consumer-app argument.

Photo & Video is also less organic than it first appears. Growth is concentrated in YouTube, Snapchat, CapCut, Canva, and other large incumbents or AI/video tools. Again, that is real app-store revenue growth, but it is not evidence that the average consumer app suddenly found game-like monetization.

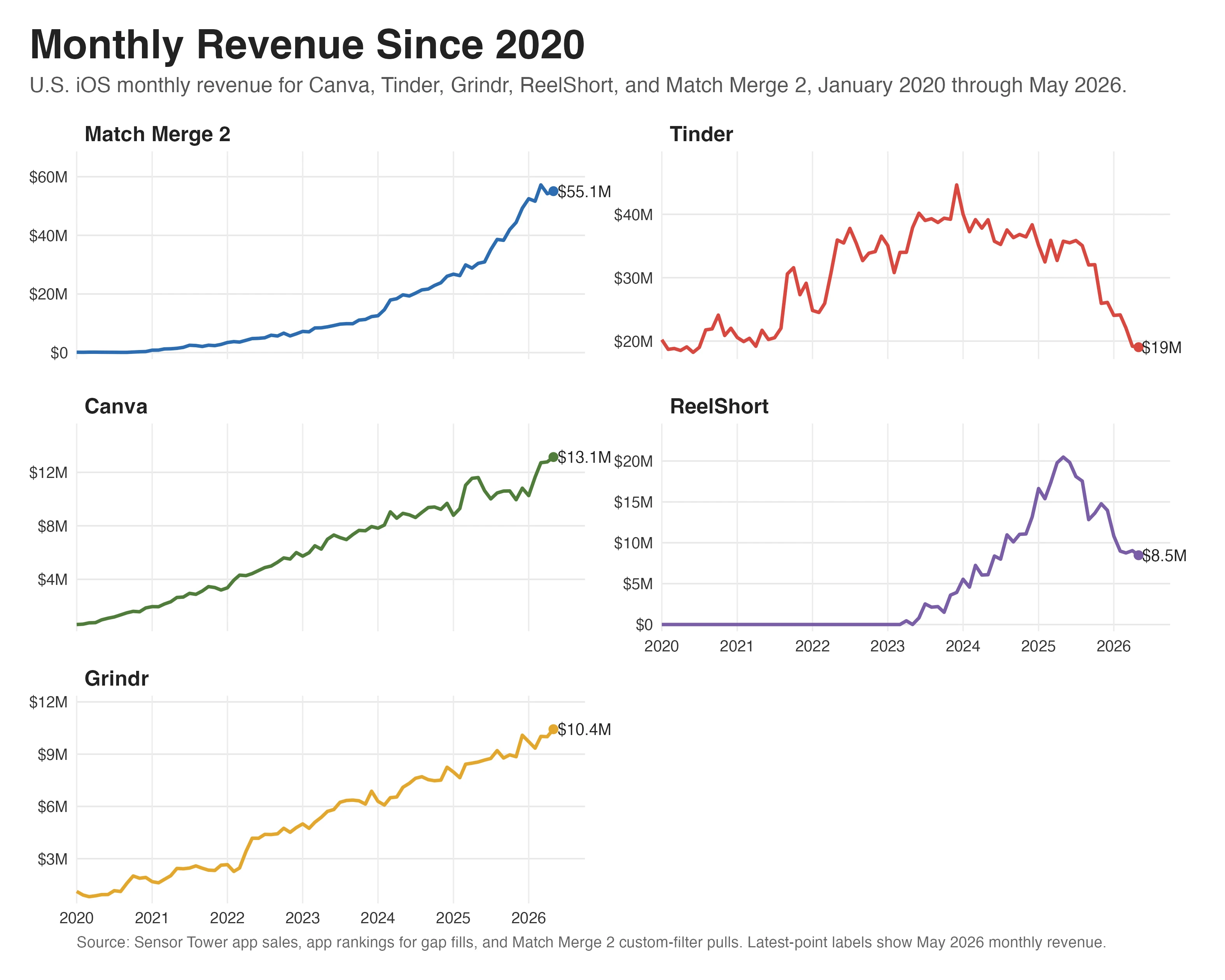

The Other category is more compelling. It includes real consumer products like Duolingo, Hinge, Tinder, Grindr, and Life360. But even after further review, growth rates pale in comparison to the time it has taken mobile games to reach comparable revenue multiples.

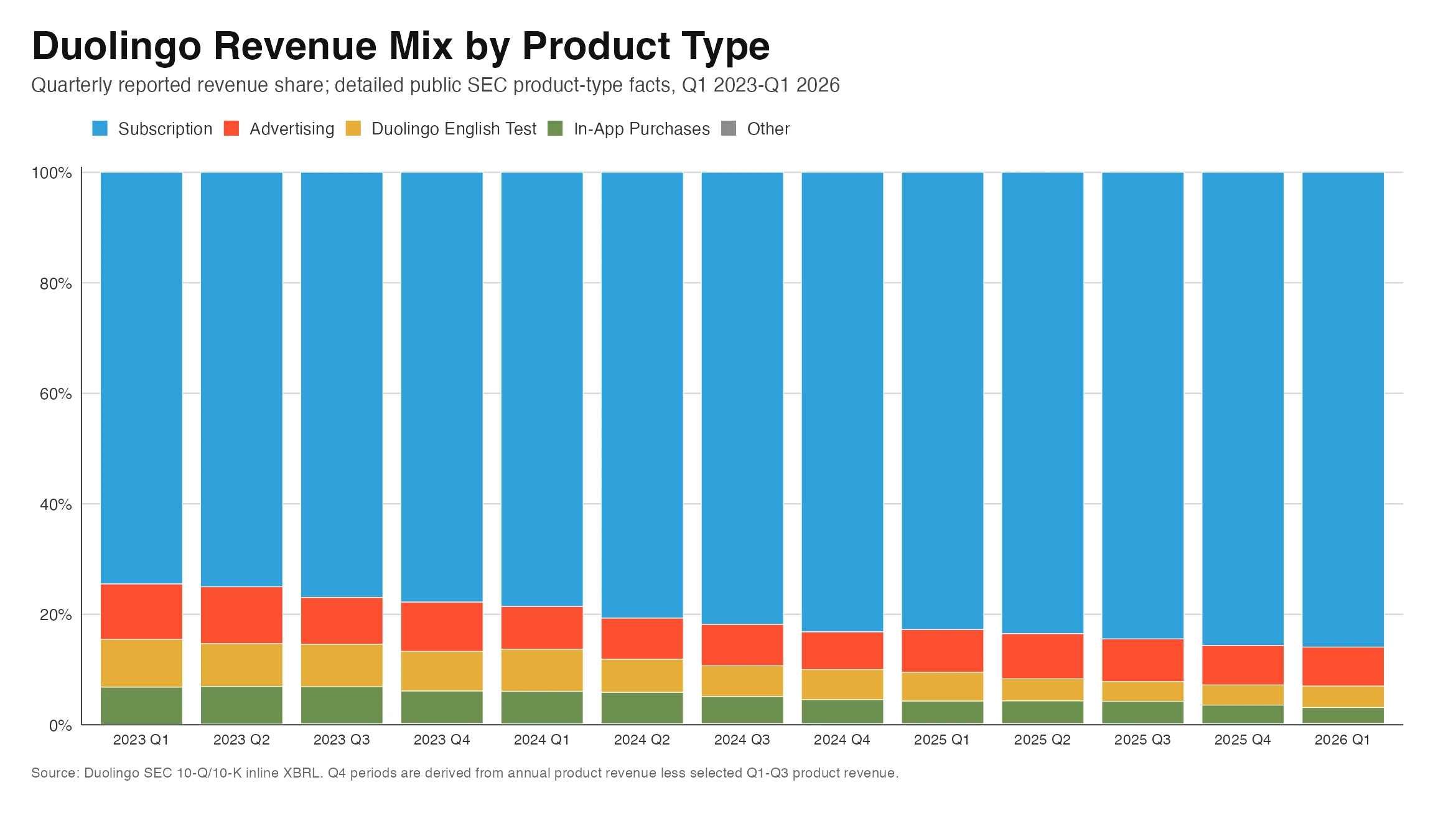

Ultimately, performance marketing is a UA growth engine. Subscriptions have been interesting, but they have also been a death sentence for Duolingo's upside because Duolingo has not built alternative revenue streams at the same depth. Subscriptions seem to have left the business price-capped as the gamification playbook has dried up.

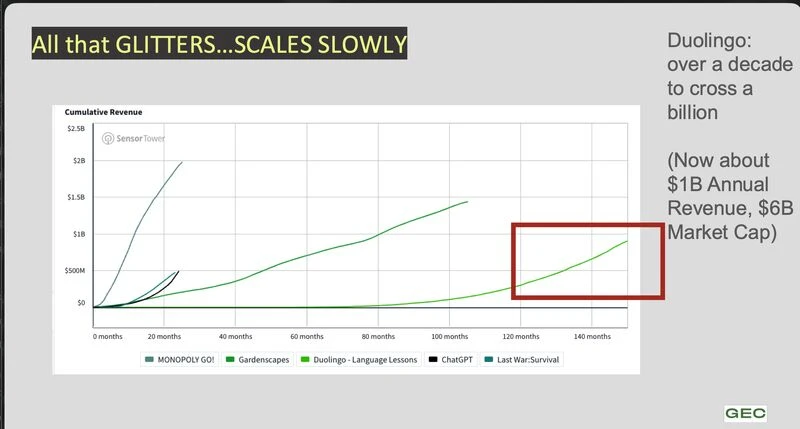

It is remarkable how quickly MONOPOLY GO! reached $1B. Duolingo took much longer. It is not clear to me that the subscription business is more resilient either. That is a common Wall Street myth, predicated on shaky assumptions about dark patterns and retention quality.

Canva, Tinder, Grindr, and ReelShort are all interesting growth cases. That is true. But even a single game subgenre, Match Merge 2, rivals them all put together. Consumer apps need to grow LTV and move beyond subscriptions to achieve game-like growth and revenue multiples.

Method note: Sensor Tower estimates are U.S. iOS consumer-spend estimates through May 2026, the latest complete month in the current pull. Other non-game apps equals Overall minus Games, Entertainment, Productivity, and Photo & Video. The top-app audit compares calendar-2025 app revenue with calendar-2020 app revenue from quarterly leaderboard pulls. The Duolingo revenue-mix chart uses public SEC filing data.